MULTI-YEAR GUARANTEED ANNUITY “MYGA”

Lock In Your Guaranteed Interest Rate

RetireMax Secure

Earn With Certainty

Get a Guaranteed Interest Rate for 3 or 5 Years.

RetireMax is a Multi-Year Guaranteed Annuity (MYGA) that provides guaranteed, predictable growth — without market risk.

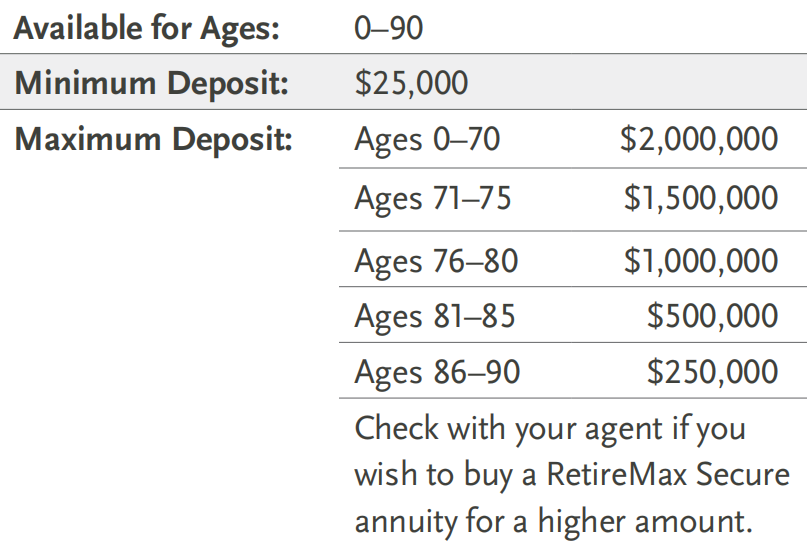

- Minimum premium: $25,000

- Higher interest rate above $100,000

- Market Value Adjustment (MVA) option with higher interest rate

- No fees or expenses, ever!

- Your money is protected With RetireMax Secure, you get a fixed interest rate. This means that you get guaranteed growth and protection from market risk.

*Withdrawal charges apply when you make early or excessive withdrawals

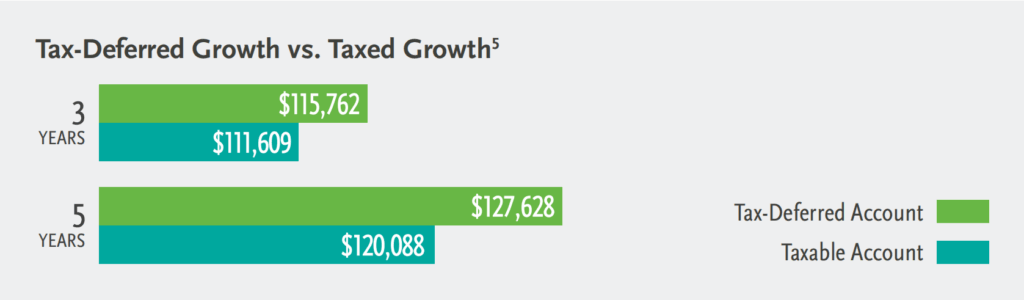

No annual taxes.

If you keep your savings in a CD or savings account, earned interest is taxable each year. With RetireMax Secure, your savings will grow tax deferred.3 That means that earned interest isn’t taxed until withdrawn.

Get a higher rate with Market Value Adjustment (MVA)

If you have an MVA version of RetireMax Secure and cash in the annuity early or make excess withdrawals, the value of your policy will be adjusted. This adjustment is based on the difference between the current 3-year or 5-year Treasury interest rate and the rate when you got the annuity.

- If the Treasury interest rate has gone down, the value is increased.

- If the Treasury interest rate has gone up, the value is reduced. The adjustment is based on the size of the rate change and on the time left in the rate guarantee period. Excess withdrawals made early will have a bigger adjustment (for the same rate change) as excess withdrawals made towards the end of the guarantee period.

The MVA versions of RetireMax Secure offer a higher guaranteed interest rate. These may be a good choice if you think that you’re likely to leave the money in the annuity for the full three or five years (or only withdraw the yearly free withdrawal amount) — in that case, your policy value is not adjusted. The MVA also doesn’t apply to the death benefit

Buying an annuity within an Individual Retirement Account (IRA) or other tax-deferred retirement plan doesn’t give you any extra tax benefits. If you’re thinking about purchasing an annuity as part of a retirement plan, base your decision on the annuity’s features and benefits, and on its risks and costs, not on tax considerations.

Annuities owned by trusts or corporate entities may not enjoy the tax-deferral feature. If you make a withdrawal before age 59½, you will be subject to a 10% federal income tax penalty unless you qualify under one of the exceptions provided by law. Some states charge a premium tax on annuities. A few states levy the tax when you pay a premium. Others charge it upon withdrawal or selection of a payment option. If we must pay this tax, we may deduct it from your policy benefits. When you receive income or make a withdrawal, you pay ordinary income taxes on the taxable value. The information in this document is based on our understanding of current tax law. You should consult your own tax advisor for tax advice.

Assumes $100,000 growing at 5% interest and a 25% tax bracket. This is a hypothetical example for illustrative purposes only and does not represent the actual results of a specific financial product

The initial annual effective interest rate is guaranteed for a set period (three or five years). After the rate guarantee period, the fixed interest rate is declared by National Life Group annually in advance. This rate is credited daily and subject to change. The company guarantees the interest rate credited to your policy will never be less than 0.25%.

With RetireMax Secure “MYGA”

you can count on knowing exactly how much money you’ll have after three or five years.

How fast can you expect your savings to grow? How much interest you’ll earn will depend on:

- The rate guarantee period (three or five years)

- The guaranteed interest rate when you buy the annuity (the rate will be higher if you opt for an MVA version)

- How much money you deposit (the rate will be higher starting at $100,000) Let’s look at an example Rate guarantee period: 5 years Guaranteed interest rate: 3.00% Deposit: $50,000 If you don’t make any withdrawals, at the end of five years, you’re guaranteed to have earned $7,963 in interest.

Of course, if you deposit more money and/or the guaranteed interest rate is higher, you’ll earn more. If you deposited $100,000 with an interest rate of 5.00%, you’d be guaranteed to earn $27,628 in interest at the end of five years (without withdrawals).

Whatever you choose to do, you’ll know exactly how much you’ll get when you buy a RetireMax Secure annuity.

Locked in, not locked out.

With RetireMax Secure “MYGA”,

You can lock in a fixed interest rate, but when you need access to cash, you have options!

Withdraw7 up to 10% annually of the accumulation value of your annuity without a withdrawal charge or Market Value Adjustment (MVA), starting in year

- Some withdrawal charges are also waived for qualifying nursing care needs or terminal illness.

- In the first year, withdrawals incur a charge (and MVA).

- Withdrawals cannot be paid back into the annuity.

- The minimum partial withdrawal you may request is $500.

- You must keep at least $5,000 in the annuity to keep it in force.

- You can set up automatic withdrawals to take out money on a regular basis.

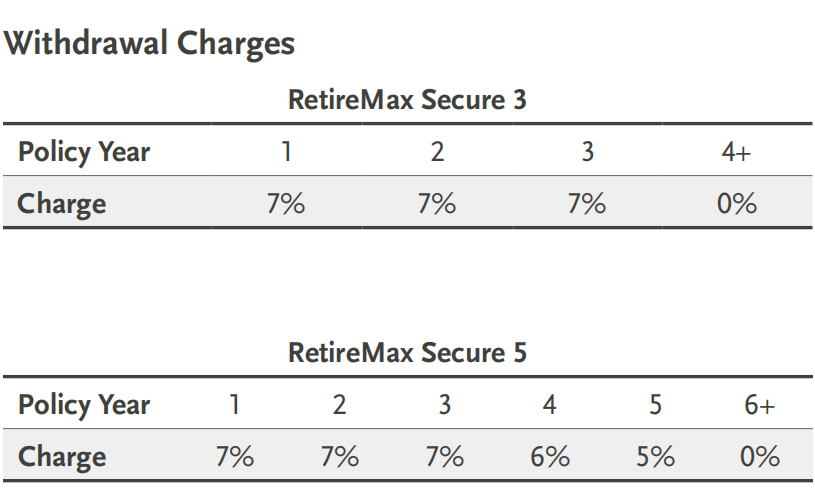

- Withdrawal charges (and MVA) do not apply to the death benefit. Withdrawal Charges If you got the annuity as part of an employer’s 403(b) or 457(b) retirement plan, you may also be able to take a loan, using your annuity as collateral, without fees or withdrawal charges

Is this annuity the right choice for me?

RetireMax “MYGA” Secure may be a good option if you’re looking to lock in a high interest rate and grow savings without paying taxes every year on earned interest. I’m looking for a secure way to grow my retirement savings.

- Lock in a guaranteed, fixed rate for predictable growth for three or five years without market risk.

- Get a higher interest rate for deposits of $100,000 or more and/or with an MVA version of RetireMax Secure. • Savings grow tax deferred — interest gained isn’t taxable until withdrawn.

- At the end of the rate guarantee period, transfer your money into another annuity without taxation, or keep the money earning interest in RetireMax “MYGA” Secure for as long as you desire at the current declared interest rate.

- Compound interest.

- No fees or expenses. I may need access to my money.

- Withdraw up to 10% of the accumulation value without a withdrawal charge (or MVA), starting in year two.

- Use the Nursing Care Rider or Terminal Illness Rider to access a portion of your accumulation value without a withdrawal charge (or MVA) if you become confined to a nursing care facility or are diagnosed with a terminal illness, starting in the second year.12 I want to spare my beneficiaries hassles and costs when I die.

- If you are the annuitant and you die while this annuity is in force, the full accumulation value will be paid to your beneficiaries without withdrawal charges (or MVA).

- Your named beneficiaries can avoid the expense, delay, and publicity of probate.

- Your beneficiaries can choose to receive the death benefit as one payment or as a series of payments over time.

Lock In a High Interest Rate Today

- Ask your agent if a MYGA is right for you.

- Choose a 3-year or 5-year guarantee period.

- Choose an MVA or non-MVA version.

- Apply with a deposit.

- Enjoy seeing your savings grow

See your policy for full details.

We believe this to be true in most states. The Iowa Insurance Division informed us that annuity contract values are includable in a probate estate in Iowa, and the attorney can charge a statutory fee against the value of the annuity contract. Consult a legal advisor in your state.

If your death occurs after periodic income payments have begun, any payments which remain to be paid under your payment option selection will be paid to your beneficiary.