INCOME DRIVER

Income Driver 10 SINGLE PREMIUM INDEXED ANNUITY

Protected From Market Risk

Ready to Grow

Predictable Guaranteed Lifetime Income

Income Driver is a single premium, fixed indexed annuity that provides predictable income for life — while protecting your principal from market loss

Get Predictable Income for Life

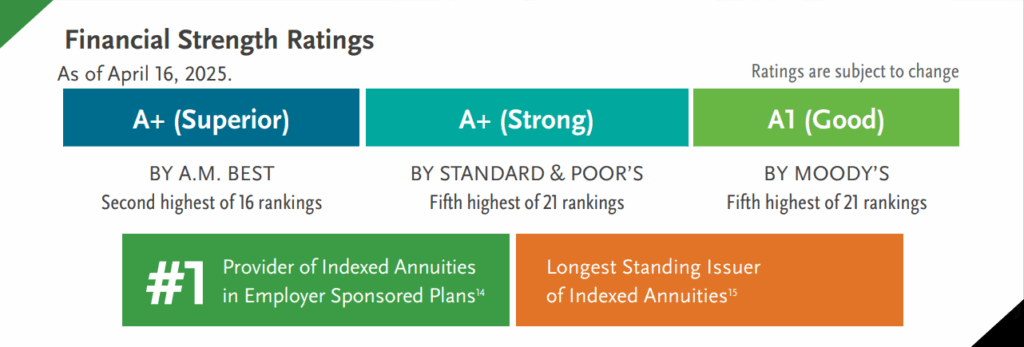

Products issued by Life Insurance Company of the Southwest®

25% Benefit Calculation Bonus with a Standard Guaranteed Lifetime Income Rider

Make your income last a lifetime. You have saved diligently for your retirement — but can you make your savings last for the rest of your life? Income Driver 10 with the Guaranteed

Lifetime Income Rider (GLIR) can help your savings become retirement income that you can never outlive, while you still retain access to the remaining cash value.

When the GLIR benefit is activated, you are guaranteed a predictable income stream for the rest of your life!

Lifetime income can start immediately

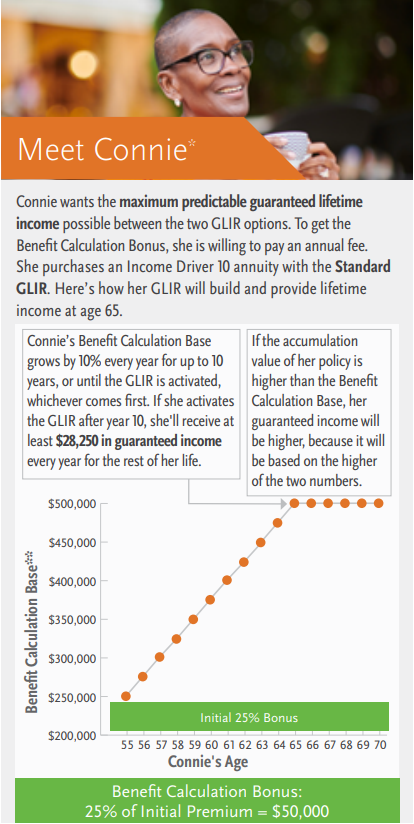

The lifetime income you receive is determined by the amount in the Benefit Calculation Base, which is not a value that can be withdrawn. The Benefit Calculation Base is boosted from the start with a 25% bonus if you choose the Standard GLIR, which has an annual charge.

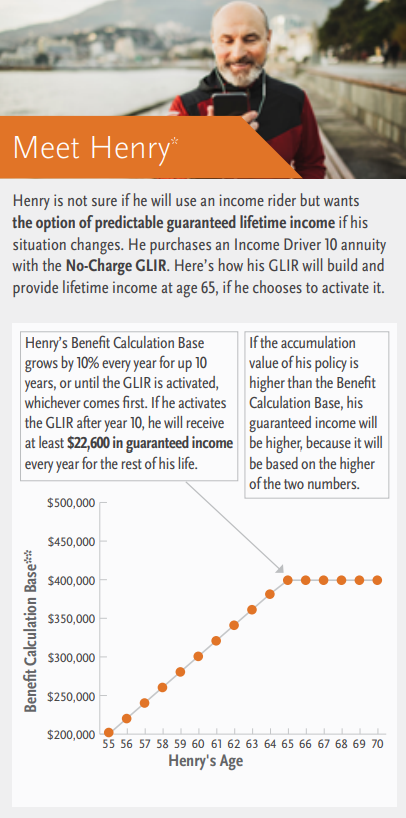

* You also have the option of a No-Charge GLIR, which does not offer a Benefit Calculation bonus. You can receive lifetime income as soon as you’re ready to activate the GLIR.

Level or increasing income

When you activate your Guaranteed Lifetime Income Rider, you can choose to get a level payment for life or an amount that will increase over time. If you select increasing income, your initial income will be lower than the level income, but your income will increase by 2.5% per year — until your accumulation value reaches zero dollars. Then, your income will lock in at the amount it has reached at that time.

Make your savings last Many seniors plan for a 20-year retirement, but for some that may result in outliving their savings. According to data from the Social Security Administration

*The Standard GLIR has a charge of 1% of the benefit base, deducted from the accumulated value annually

Choose the GLIR that's right for you

Both the Standard GLIR and the No-Charge GLIR provide a guaranteed lifetime income. You can choose the GLIR that works best for you when you purchase the Income Driver 10 annuity

No-Charge GLIR

The No-Charge GLIR Benefit Calculation Base builds at an 10% simple roll-up rate until you activate the GLIR or after 10 years, whichever comes first.

Standard GLIR

The Standard GLIR credits an upfront 25% bonus to the Benefit Calculation Base. Then, the Benefit Calculation Base grows at a 10% simple roll-up rate until you activate the GLIR or after 10 years, whichever comes first.

Double your income when you need it most. Both of the GLIR options offer Income Doubler, which you can use if you become incapacitated. With Income Doubler, your income can be doubled for up to five years if:

- Your policy has been in force for two years.

- You cannot perform two of the six activities of daily living without the assistance of another individual, who is permanently helping you with: – Bathing– Dressing– Transferring– Toileting– Continence – Eating

- Your policy has an accumulation value greater than zero dollars.

- The elected income is based on one life only.

- No withdrawals in excess of the current lifetime income have been taken in the current policy year. If Connie qualifies for the Income Doubler, her income for the next five years will double from $28,250 to $56,500

How your retirement savings can grow. To make sure you’re in the best position possible before drawing a lifetime income stream, Income Driver 10 gives you multiple options to grow the value of your annuity. You can choose a fixed rate or opt for getting interest credited based on the growth of a market index of your choice — without directly participating in the market.

Available indexes You have the choice between three market indexes

S&P 500® Index The S&P 500® is widely regarded as the best single gauge of the U.S. equities market. This world-renowned index includes a representative sample of 500 leading companies in leading industries of the U.S. economy. Although the S&P 500® focuses on the large-cap segment of the market, it is also an ideal proxy for the total market.

US Fundamental Balanced Index This index aims to minimize volatility through a blend of U.S. equities, U.S. treasuries, and cash. The asset classes are rebalanced daily to seek to minimize risk and the mix of U.S. equities is revised quarterly. This index was created and is owned by PIMCO.

Global Balanced Index This index aims to enhance risk-adjusted returns by tracking a blend of global asset classes: equities, bonds, and commodities. The index composition is rebalanced among asset classes monthly based on the SG Sentiment Indicator. This indicator is made up of six cross-asset market risk measures. The overall allocation is then reviewed daily to reduce market exposure in case of high volatility. This index was created and owned by Société Générale

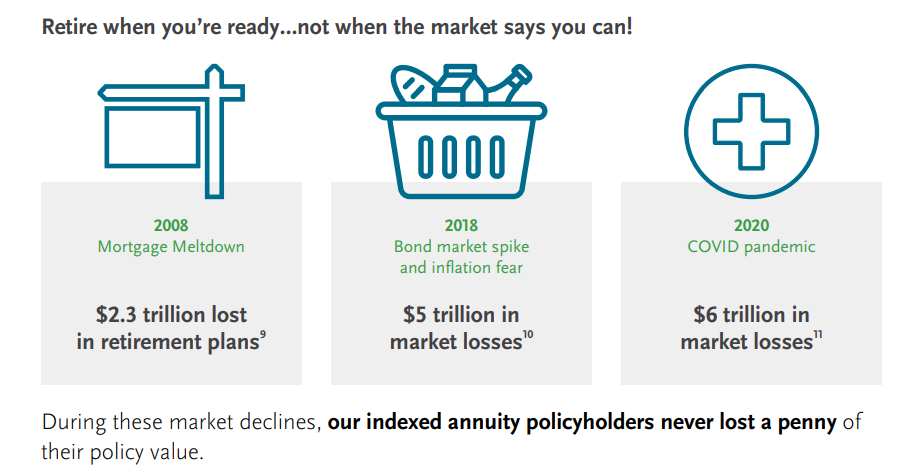

Never lose a penny. As the longest standing issuer of indexed annuities, National Life Group has seen many stock market upswings and downturns. As retirement gets closer, volatility is a worry for many, because there’s not much time to recover from market losses.

The good news is that you’re not exposed to this risk because indexed annuities do not directly participate in any stock or equity investment, and you can never get less than 0% interest in any given period. That means that you can grow your retirement savings when markets do well — and never lose a penny of your interest earned and premium paid when markets fall

As with all Investment vehicles there is a decreasing surrender charge, an equal standard feature even if retaining a CD from a financial institution.

Upside Potential

Grow the value of your policy.

• Diversify with multiple index crediting options, including a performance trigger option, which credits interest as long as the index did not lose value.

• Ask your financial professional about which options best suit your needs.

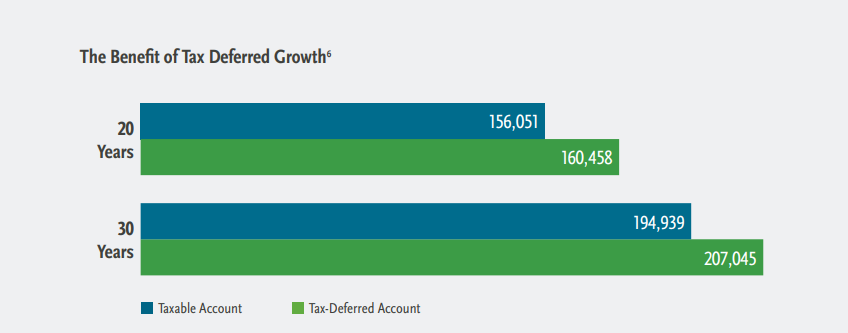

Tax-Deferred Growth

• Your money can potentially earn interest and grow tax deferred until withdrawn or received as income.

• Annuities owned by trusts or corporate entities may not enjoy tax deferral.

Downside Protection

Avoid market losses.

• Never lose a penny.*

• The least interest you are ever credited is 0%.

What Happens After I Die?

With Income Driver 10, your named beneficiaries can avoid the expense, delay, and publicity of probate. If you are the Annuitant and you die while this annuity is in force, the full accumulation value will be paid to your beneficiary without withdrawal charges.